INTRODUCTION

The objective of this Technical Accounting (TA) Alert is to:

- provide information regarding the Accounting Standards (and Interpretations) that have been issued with an effective date post 30 June 2023; and

- assist entities in meeting the disclosure requirements in paragraph 30 of AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors.

OVERVIEW

When the AASB issues a new or revised Standard (or an Interpretation)1 with an effective date after the end of the reporting period, an entity2 has a choice of either:

- early adoption of the Standards in accordance with section 334(5) of Corporations Act 2001 (via a Director’s minute – an example is included in this Alert) and disclosing this fact in the financial statements; or

- not adopting the Standard; in which case the entity must comply with paragraph 30 of AASB 108.

Requirements of paragraph 30 of AASB 108

30 When an entity has not applied a new Australian Accounting Standard that has been issued but is not yet effective, the entity shall disclose:

- this fact; and

- known or reasonably estimable information relevant to assessing the possible impact that application of the new Australian Accounting Standard will have on the entity’s financial statements in the period of initial application.

Furthermore, paragraph 31 of AASB 108 states that in complying with paragraph 30 an entity should consider disclosing:

- the title of the new Australian Accounting Standard;

- the nature of the impending change or changes in accounting policy;

- the date by which application of the Australian Accounting Standard is required;

- the date at which the entity plans to apply the Australian Accounting Standard initially; and

- either:

-

- a discussion of the impact that initial application of the Australian Accounting Standard is expected to have on the entity’s financial report; or

- if the impact is not known or reasonably estimable; a statement to that effect.

Standards and Interpretations with an effective date post 30 June 2023

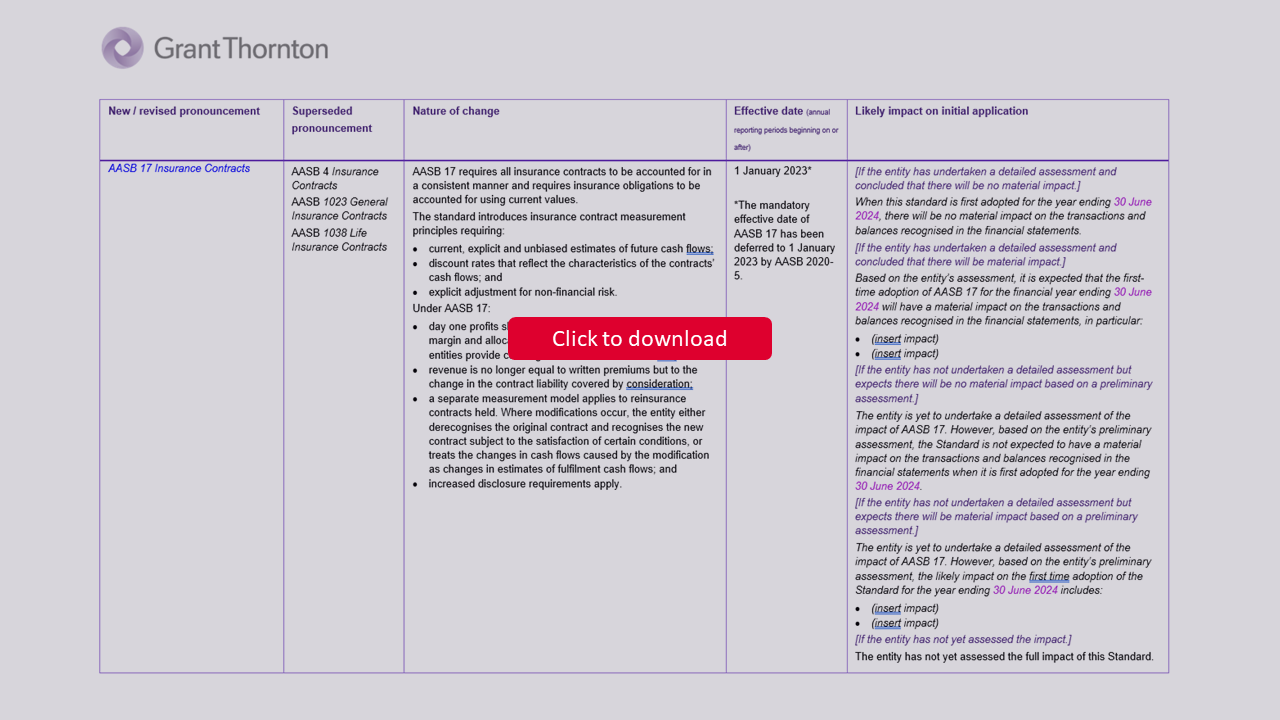

The table following (pages 3 - 8) summarises all Accounting Standards (and Interpretations) that have been issued by the AASB and IASB as at 8 May 2023. Any further Standards (and Interpretations) issued after this date will also need to be disclosed up until the date of authorisation of the financial report.

Although the table lists most of the Standards (and Interpretations) issued but not yet effective, entities should only disclose Standards (and Interpretations) that are relevant to them. For instance, a for-profit entity does not need to disclose the impact of a new Standard that only applies to entities in the not-for-profit sector.

In addition, it is important that the sample disclosure/indicative impact for each Standard and Interpretation is tailored to suit the particular circumstances of each entity. Entities should pay particular attention to this disclosure, noting that the Australian Securities and Investments Commission (ASIC) has been expressing concerns over several years with entities providing ‘boilerplate’ disclosures. The document Globally consistent reporting for sustainability-related information may be of particular assistance where disclosure is influenced by sustainability-related factors.

Entities applying Australian Accounting Standards – Simplified Disclosures (SD)

Tier 2 entities reporting under the Simplified Disclosure (SD) regime are not required to disclose Accounting Standards issued but not yet effective. Accordingly, no SD-related amendments have been included in the table. Given the relative significance of different standards not yet effective, entities may choose to make related disclosures on an optional basis. We encourage entities to consider disclosure where the impact is potentially material.

Early adoption of Standards

Where Standards or Interpretations are adopted early, the following Director’s minutes may be used for Corporations Act entities3:

“In accordance with s334(5) of the Corporations Act, the Directors are early adopting the following Accounting Standards:

- AASB xxxx

- Interpretation yy”

Please click the table below to download.

![]()

Click here to download this table.

ACTION REQUIRED

With the 30 June 2023 reporting season commencing, entities should now take time to review and consider the impact of new and revised accounting standards that have been issued but are not yet effective. This is particularly important considering that ASIC is looking to scrutinise disclosures in this area.

Footnotes

- Where an entity includes an explicit and unreserved statement of compliance with International Financial Reporting Standards (IFRSs) as required by paragraph 16 of AASB 101 Presentation of Financial Statements, the entity needs to consider Standards issued by the IASB but not yet issued by the AASB. This is likely to apply to all entities, except for those issuing special purpose financial statements and not-for-profit entities.

- The requirements of paragraph 30 of AASB 108 are mandatory for all entities preparing financial statements under Part 2M.3 of the Corporations Act 2001 and for those preparing general purpose financial statements (excluding entities applying Australian Accounting Standards – Simplified Disclosures).

- Section 334(5) of Corporations Act 2001 states that a company, registered scheme or disclosing entity may elect to apply the Accounting Standard to an earlier period unless the Standard says otherwise. The election must be made in writing by the Directors.