Developing strong sustainability reporting processes for voluntary and mandatory sustainability reporting.

In Australia, environmental considerations are gaining importance, particularly as the Federal Government has legislated an emissions reduction target of 43 per cent below 2005 levels by 2030, with a commitment to achieving net-zero emissions by 2050.

In addition, certain entities will be required from 1 January 2025 to prepare an annual sustainability report as part of the annual report, providing decision useful information for investors about climate-related risks and opportunities that could be reasonably be expected to affect an entity’s cashflows, access to finance, or cost of capital over the short, medium, and long term. This statutory sustainability report will require compliance with the new standard AASB S2 Climate-related Disclosures.

Additionally, across value chains and supply chains, organisations are increasingly being asked to provide sustainability-related information to their customers, creditors or other third-parties as part of doing business.

There is often an expectation that CFOs and finance teams will be across a whole range of new sustainability reporting frameworks and standards, many of which require new skill sets and specialist expertise in an already resource-constrained environment – which we can provide.

As the reporting requirements become increasing regulated and more entities are developing their capabilities in this area, it is important you receive the most practical and least disruptive support to ensure your reporting meets the needs of stakeholders whilst allowing you to focus on running your business.

Who is caught by Australian statutory sustainability reporting?

Recent legislative changes now require preparation of an annual sustainability report for entities meeting certain criteria

- Entities that prepare annual reports under Chapter 2M of the Corporations Act; and

Either

- Meet any two of three thresholds as shown in the table below; or

- Are a registered corporation under the NGER Act, or an entity required to register under the NGER Act; or

- Are a registered scheme, registrable superannuation entity, or retail corporate collective investment vehicle (CCIV), with consolidated assets in excess of the threshold shown in the table below.

NB - The criteria for entities in scope of the legislation is contained in section 292A of the Corporations Act. If you are not certain if your organisation is in scope of the legislation, please seek legal advice.

![]()

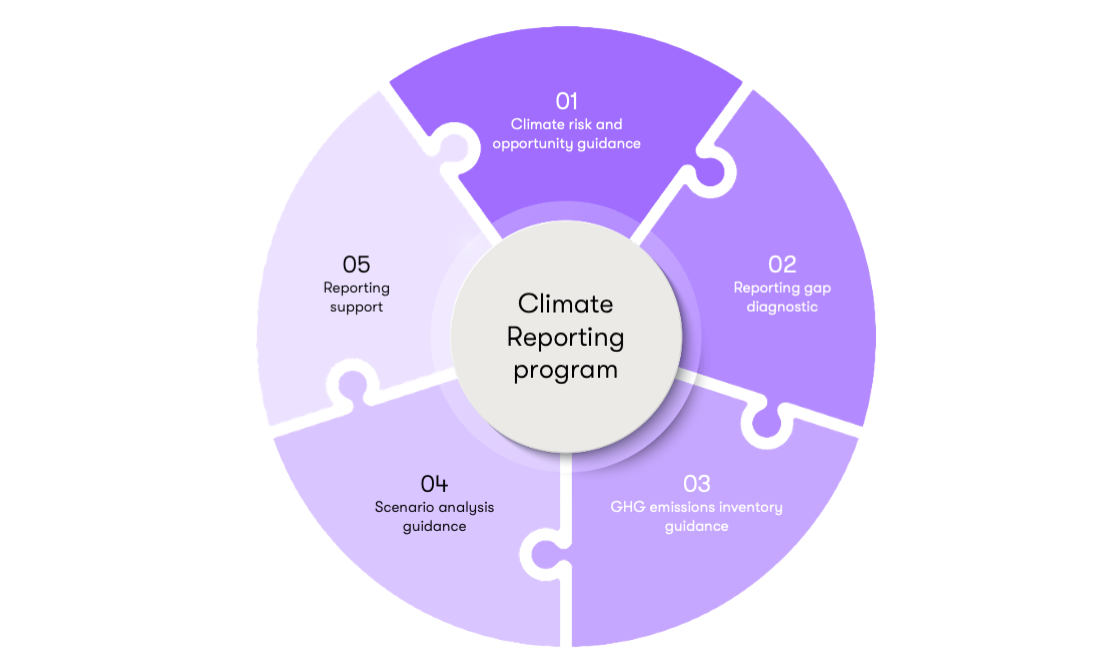

Preparing your sustainability report

Grant Thornton has a team of specialists who understand the rapidly developing landscape of sustainability reporting and will work closely with you to navigate through the process of collating the right information, building appropriate processes and controls around the data required to support disclosures, and how to present the required information.

We offer a range of services including:

- Education and training on sustainability reporting requirements (Australia or internationally)

- Support with identification of and horizon scanning for international sustainability reporting obligations

- Support with the identification of climate-related and sustainability-related risks and opportunities in your business model or value chain

- Assessing your current capabilities against the requirements of a particular framework, or general best practices in voluntary reporting

- Support with undertaking a climate scenario analysis

- Support with developing your greenhouse gas (GHG) emissions inventory and subsequent transition planning

We also understand the importance of aligning your current practices with the relevant sustainability standards to ensure the information you present in your sustainability report is best practice, is clear and concise, and is suitable for assurance.

Get in contact with our sustainability experts to learn more about how we can help you develop strategies, meet the standards, and produce rigorous reporting.