INTRODUCTION

AASB 2021-2 Amendments to Australian Accounting Standards – Disclosure of Accounting Policies and Definition of Accounting Estimates amends five Australian Accounting Standards regarding the disclosure of accounting policies and definition of accounting estimates as a result of amendments made to International Financial Reporting Standards.

AASB 2021-6 Amendments to Australian Accounting Standards – Disclosures of Accounting Policies: Tier 2 and Other Australian Accounting Standards amends three Australian-specific standards as a consequence of AASB 2021-2.

The amendments, which apply prospectively to annual reporting periods beginning on or after 1 January 2023, and their impacts are summarised below.

OVERVIEW

Disclosure of accounting policies

What is the change?

AASB 2021-2 amends AASB 1011, AASB 72 and AASB 1343 to require disclosure of ‘material accounting policy information’ rather than ‘significant accounting policies’ in an entity’s financial statements. It also updates AASB Practice Statement 2 to provide guidance on the application of the concept of materiality to accounting policy disclosures.

AASB 2021-6 amends AASB 10494 and AASB 10605 to require disclosure of ‘material accounting policy information’ rather than ‘significant accounting policies’ in an entity’s financial statements. It also amends AASB 10546 to reflect the updated terminology used in AASB 101 as a result of AASB 2021-2.

Why the change?

This change resulted from the fact that the term ‘significant’ is, unlike the term ‘material’, not defined in Australian Accounting Standards or other authoritative literature. The absence of definition gave rise to difficulties in assessing whether accounting policies were required to be included, resulting in diversity in practice.

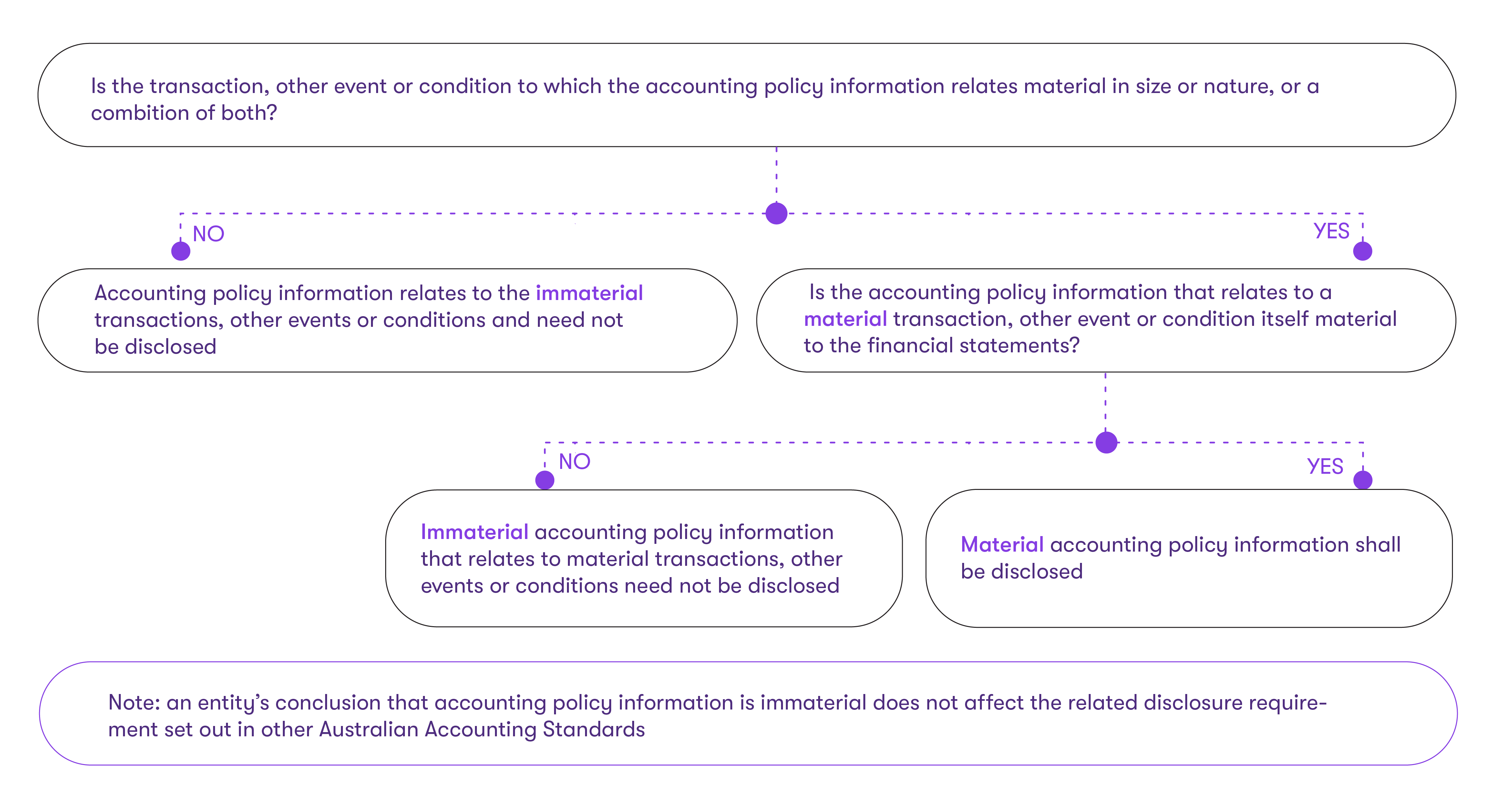

What is meant by material?

AASB 101 paragraph 7 defines information as being material if “omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general-purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity”.

In determining whether information is material, an entity should consider the nature or magnitude of information, or both, including whether omission of the information would be important to the understanding of the financial statements by users.

The following diagram can assist when determining whether accounting policy information is material.

![]()

Download diagram

What are material accounting policies?

The information contained within accounting policy disclosures is useful to a user’s decision making when they:

- Relate to material transactions, other events or conditions;

- Provide insight into how an entity has exercised judgement in selecting and applying accounting policies;

- Contain entity-specific information rather than standardised information; and

- Do not merely duplicate or summarise the content of the recognition and measurement requirements of the Accounting Standards; although sometimes this information is material if:

- it is needed to understand other material information in the financial statements – for example, in applying AASB 9 regarding the classification of financial instruments;

- an entity reports in a jurisdiction in which entities also report applying local accounting standards; or

- the accounting required by the accounting standards is complex, and users of the financial statements need to understand the required accounting.

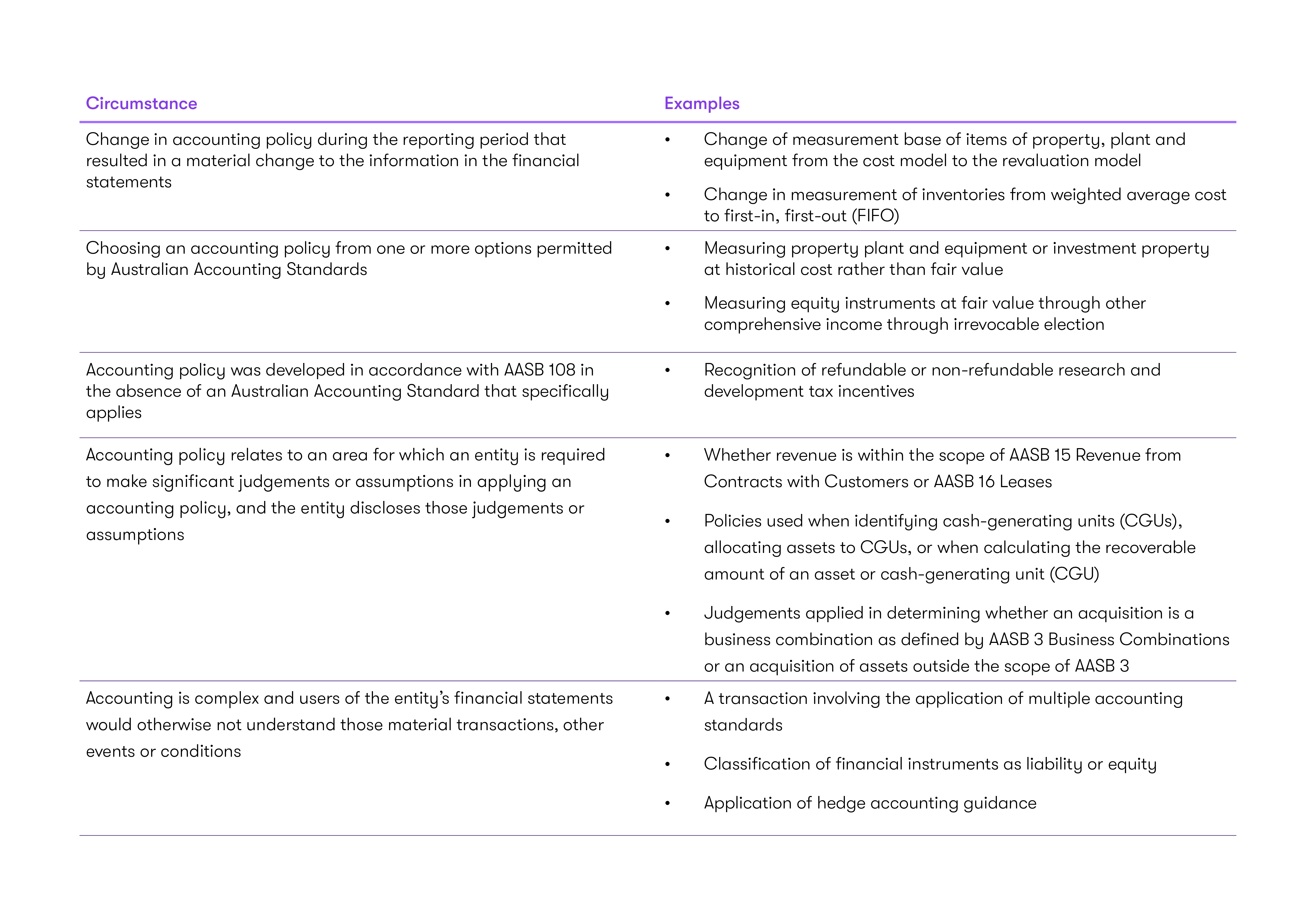

The following are examples of circumstances that would generally give rise to what would be considered, a material accounting policy:

![]() Download table

Download table

Who is expected to be impacted by the change?

The amendment is expected to have a greater impact on entities whose financial statements contain disclosures that are not entity-specific as disclosures that contain material accounting policies only contain entity-specific rather than standardised information – for instance, many entities will not require policies for hedge accounting or amortised cost receivables other than trade receivables.

Definition of accounting estimates

What is the change?

The amendment replaces the definition of a ‘change in accounting estimate’ in paragraph 5 of AASB 108 with the definition of ‘accounting estimates’. The amendment also clarifies that, a change in accounting estimate does not relate to prior periods and is not the correction of an error unless it resulted from the correction of a prior period error.

Why the change?

Some users found it difficult to distinguish between a change in accounting policy and change in accounting estimate. The new definition seeks to make that distinction clearer.

What is an accounting estimate?

An accounting estimate is defined as “monetary amounts in financial statements that are subject to measurement uncertainty”.

Measurement uncertainty is the measurement of monetary amounts that cannot be observed directly and must instead be estimated.

Examples of accounting estimates include:

![]()

Download table

What causes a change in accounting estimate?

Accounting estimates can change as a result of the following:

![]()

Download table

The above circumstances result in a change in accounting estimate and do not give rise to a change in accounting policy or the correction of a prior period error because:

- the accounting policy remains the same; and

- the value of the estimate has changed at reporting date based on current facts and circumstances through a change in measurement technique and/or inputs used in the measurement technique applied.

Who is expected to be impacted by the change?

The amendment is not expected to have a significant impact on entities as it is a narrow-scope amendment which clarifies the definition but is not expected to result in a change in practice.

Footnotes

1 AASB 101 Presentation of Financial Statements

2 AASB 7 Financial Instruments: Disclosures

3 AASB 134 Interim Financial Reporting

4 AASB 1049 Whole of Government and General Government Sector Financial Reporting

5 AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities

6 AASB 1054 Australian Additional Disclosures