What are the changes?

Effective for annual reporting periods beginning on or after 1 January 2022, AASB 116 prohibits entities from deducting from the cost of an item of Property, Plant and Equipment, any proceeds from selling items produced while bringing property, plant and equipment to the location and condition necessary for it to be capable of operating in the manner intended by management. Instead, sales proceeds and related costs are required to be recognised in profit or loss.

The definition of ‘costs of testing whether the asset is functioning properly’ has also been clarified, with the definition now including the context of “assessing whether the technical and physical performance of the asset is such that it is capable of being used in the production or supply of goods or services, for rental to others, or for administrative purposes”.

The amendment was introduced to remove the observed diversity in practice whereby entities were either deducting from the cost of its property, plant and equipment, or recognising directly in profit or loss, those proceeds generated while bringing that asset to the location and condition necessary for its intended use, in turn improving the comparability of financial statement information. The amendment also serves to introduce greater alignment with similar principles contained within AASB 138 Intangible Assets.

Who is impacted?

The amendment applies to all entities, however is expected to more significantly impact the extractive, petrochemical and manufacturing industries.

What was prior practice?

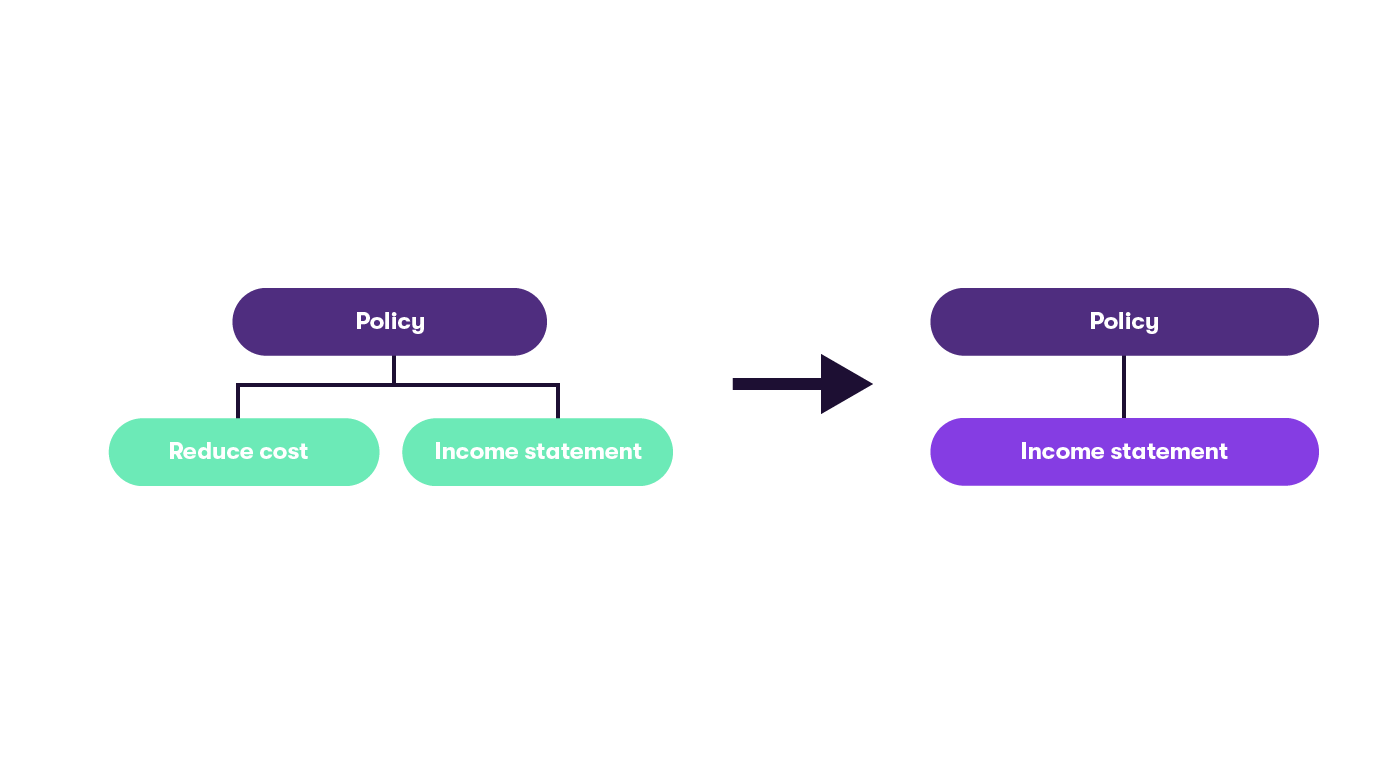

In the absence of specific principles, entities generally followed one of two different policies:

- Recognise proceeds in profit or loss

- Recognise proceeds as a reduction in the cost of the associated property, plant and equipment.

![]()

How should the proceeds be recognised in profit or loss?

The amendments require proceeds to be recognised in profit or loss ‘in accordance with the applicable Standards’ (AASB 116.20A). Therefore, if an item of property, plant and equipment is producing outputs (i.e. inventory) that would be sold in the entity’s ordinary course of business, the proceeds would likely be recognised in accordance with AASB 15 Revenue from Contracts with Customers – this will be assumed for the remainder of this document. While intuitive as an outcome, entities must carefully consider whether AASB 15 applies given the facts as it relates to their ordinary activities. This results in additional complication when considering the costs associated with the transaction:

- AASB 15 Revenue from Contracts with Customers requires that the costs associated with a satisfied performance obligation be expensed; and

- AASB 102 Inventories requires that inventories be measured at cost, including “costs of conversion and other costs incurred in bringing the inventories to their present location and condition,” and be recognised as an expense “when inventories are sold”.

Judgement is required to be applied when applying these standards.

How should the associated costs of inventories be recognised?

Types of costs incurred

In practice, it is acknowledged that a variety of costs may be incurred while bringing an item of property, plant or equipment to the location and condition necessary for its intended use. In such circumstances, entities should apply judgement and refer to the guidance in existing standards to determining the most applicable standard and treatment. Examples include:

Cost

|

Accounting Standard

|

Treatment

|

| Costs directly attributable to construction of an item of property, plant and equipment |

AASB 116.16(b)

|

Include in the cost of an asset |

| Costs of bringing inventories to their present location and condition |

AASB 102.10, .12-.14 |

Include in cost of inventories

Recognise in profit or loss at the time inventories are sold

|

| Costs excluded from the cost of inventories – e.g. abnormal amounts of wasted materials, labour or other production costs |

AASB 102.6 |

Recognise in profit or loss as an expense in the period in which they are incurred where abnormal costs are not in relation to testing of property, plant and equipment |

| Costs of stripping activity assets and costs of inventories produced during the production phase of a surface mine |

Interpretation 20.8 |

To the extent that the benefit from the stripping activity is realised in the form of inventory produced, account for the costs in accordance with AASB 102

Recognise cost of stripping activity that improves access to ore as an addition to, or enhancement of, another non-current asset

Otherwise, recognise as an expense in the period in which they are incurred

|

| Administrative, marketing or staff training costs |

AASB 116.19 |

Recognise in profit or loss as an expense in the period in which they are incurred |

| Costs of using or redeploying property, plant and equipment |

AASB 116.20 |

Recognise in profit or loss as an expense in the period in which they are incurred |

| Costs of incidental operations |

AASB 116.21 |

Recognise in profit or loss as an expense in the period in which they are incurred |

AASB 102.10 requires an entity to include the cost of conversion in the cost of inventories, including depreciation of associated property, plant and equipment. Judgement must be applied, however it is likely that no depreciation of the property, plant and equipment being used in production of the incidental inventory would be included within the cost of inventory produced as the asset(s) producing those items is not available for use (AASB 116.55).

Implications when excess direct costs are incurred

In some instances, costs incurred in conversion of inventories may exceed the costs normally expected after commencement of operation of property, plant and equipment. Such costs may indicate, variously:

- costs that are incidental in nature;

- costs that are abnormal in nature (due to inefficiencies); or

- costs that are associated with establishment of the items of property, plant and equipment that were incorrectly capitalised.

AASB 2020-3 amends AASB 116 such that it explicitly states that cost of the items produced must be measured applying AASB 102. The operation of AASB 102 as it relates to these costs requires that, for inventory on-hand at reporting date, any excess carrying value of an item of inventory above net realisable value ("NRV") be recognised as expense. The cost of any items of inventory consumed during the period (for instance, through sale) is required to be recognised as an expense (AASB 102.34), with the exception of any items utilised as a component of self-constructed property, plant and equipment (AASB 102.35).

For example, an entity may have incurred labour and other production costs in excess of the potential NRV of the item of inventory being produced. Such excess is included in the cost of inventories until sale or reporting date, at which point it is either recognised as cost of sales or recognised as a reduction in carrying value to NRV through expense. If the excess costs incurred are of a nature such that they would be considered ‘abnormal amounts of wasted materials, labour, or other production costs’, or similar, they are expensed as incurred (AASB 102.16).

Considerations at reporting date

Where costs incurred result in the recognition of inventories under AASB 102, entities shall consider whether any reduction in carrying value of inventories to net realisable value is required, with any losses recorded in profit or loss as an expense in the period in which the write-down occurs.

Disclosure Requirements

If such proceeds and costs are not presented separately in the statement of comprehensive income, an entity shall disclose:

- The amounts; and

- The line item(s) in the statement of comprehensive income that includes such amounts.

Example – Presentation of income

Entity A is constructing a facility which produces widgets, a product which Entity A currently produces in other locations. Widget production is highly automated, involving multiple discrete processes completed in stages. Inventory completed at each stage is able to be stockpiled and utilised at a later date.

During the testing phase of construction, Entity A produces 1,500 widgets. 500 widgets are produced with flaws and have no salvage value. 1,000 widgets of saleable quality are produced. $400,000 is received upon sale of the widgets.

Entity A applies AASB 15 Revenue from Contracts with Customers and recognises $400,000 in accordance with that standard1.

Example – Presentation of costs incurred

Assume the same facts as the above example, except that production of widgets occurs in the reporting period prior to sale of widgets, in addition to the below.

During the testing phase of construction, Entity A incurred certain costs. In assessing the costs incurred, it applied various standards to determine the presentation of each in the financial statements.

Cost incurred

|

Paragraph applied

|

Presentation

|

Explanation

|

| Engineering consultants – monitoring of process |

AASB 116.16 |

Element of cost of PPE |

Item identified in AASB 116.17 as directly attributable cost. Engineers are not required to be on-hand during future production. |

| Unsaleable product |

AASB 102.16 |

Expense |

Note 1 |

| Costs of storage |

AASB 102.16 |

Expense |

Explicitly identified |

| Inventory input costs |

AASB 102.11 |

Element of inventory |

Note 2 |

Note 1: Judgement must be applied as to whether unsaleable product is produced as an ‘wasted materials’ and expensed as per AASB 102.16, or a directly attributable cost that is ‘testing’ in nature and therefore recognised as an element of cost of property, plant and equipment as required by AASB 116.17(e).

Note 2: To the extent not considered ‘excess waste’, AASB 102 requires that the costs of purchase and conversion of raw materials be included as inventory. Judgement will be required to ensure that excess wastage – for instance, additional labour for certain yet-to-be-automated processes are appropriately allocated to expense.

After completing the allocation of value, Entity A determines that the cost of each widget is $500 and all costs of selling of each item of inventory will total $50. Entity A therefore impairs the items of inventory to $350 by reference to the selling price ($400) less costs to sell ($50).

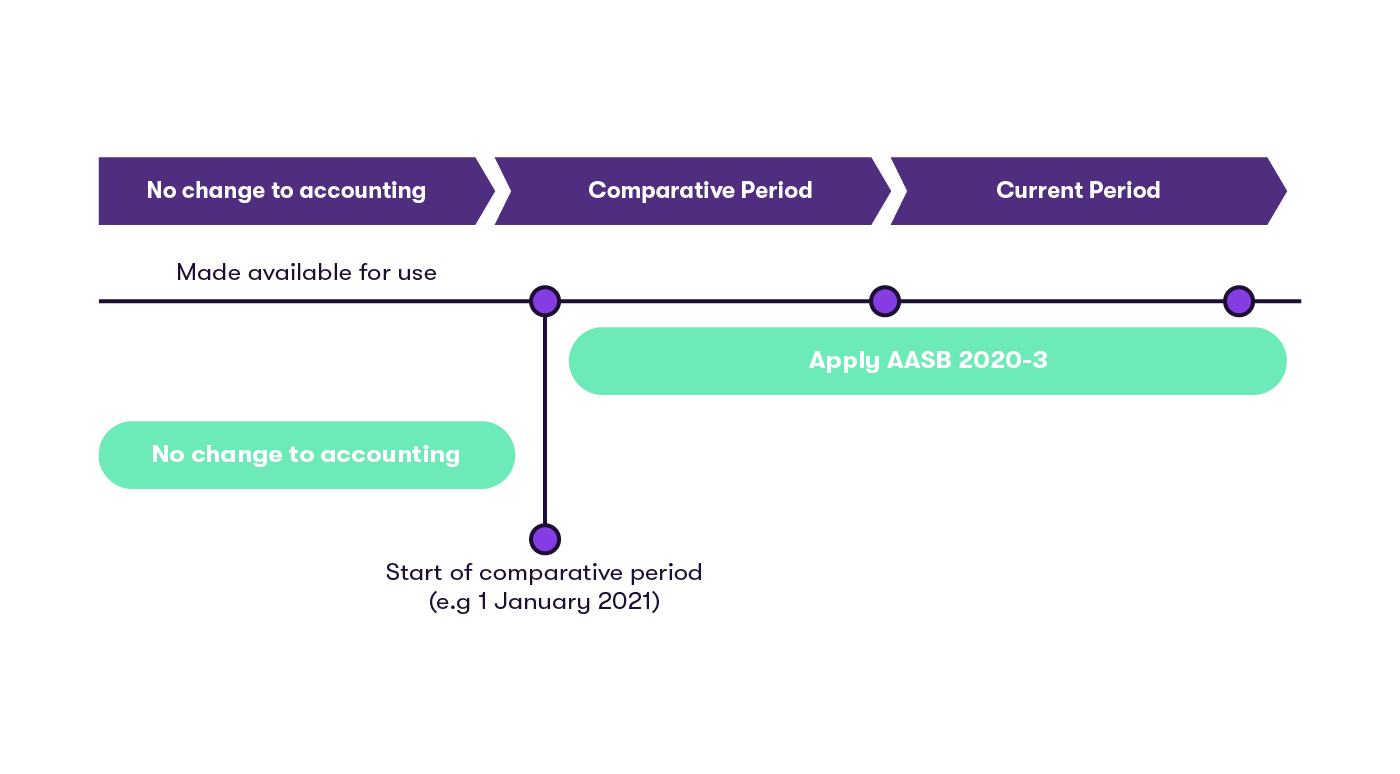

Transitional requirements

The amendment is to be applied retrospectively, to all assets which were made available for use at the beginning of the earliest comparative period presented in the financial statements in which the entity first applies the amendment. Therefore, if an entity has a 31 December 2022 year end, any assets which were made available for use from 1 January 2021 onwards must comply with the amendments in AASB 2020-3.

![]()

The cumulative effect (if any) of applying this amendment is taken to opening retained earnings at the beginning of that earliest period presented.

Footnotes

1. The application of AASB 15 is often of significantly greater complexity than identified in this example. We recommend the completion of a detailed analysis.