INTRODUCTION

The purpose of this Alert is to draw attention to the Australian Sustainability Reporting Exposure Draft ED SR1 (ASRS Exposure Draft) published by the Australian Accounting Standards Board (AASB) in October 2023.

This is the first public draft of the Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information. There are three draft standards:

- [Draft] ASRS 1 General Requirements for Disclosure of Climate-related Financial Information;

- [Draft] ASRS 2 Climate-related Financial Disclosures, and

- [Draft] ASRS 101 References in Australian Sustainability Reporting Standards.

The exposure drafts of ASRS 1 and ASRS 2 are substantially aligned to the IFRS Sustainability Disclosure Standards issued by the International Sustainability Standards Board (ISSB) in June 2023:

- IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information; and

- IFRS S2 Climate-related Disclosures.

The AASB developed [draft] ASRS 1 and [draft] ASRS 2 based on consideration of Treasury’s Climate-related Financial Disclosure: Consultation Paper (June 2023) (Treasury’s second consultation paper on the subject) and informal feedback from stakeholders, including staff members of Treasury, the Australian Government Department of Climate Change, Energy, the Environment and Water (DCCEEW) and the CSIRO.

The proposals in the ASRS Exposure Draft are subject to change based on Treasury’s Climate-related Financial Disclosure: Exposure draft legislation (January 2024), and final amendments to that legislation.

Comments on the ASRS Exposure Draft close on 1 March 2024.

OVERVIEW

The ASRS Exposure Draft was developed by the AASB considering the commitment from the Australian Government to introduce internationally-aligned mandatory climate-related financial reporting for large businesses and financial institutions and the request for comment process associated with the IFRS Sustainability Disclosure Standards setting process. The AASB decided:

- to develop Australian sustainability-related reporting requirements as a separate suite of standards to Accounting Standards;

- to use the work of the ISSB as a foundation, with modifications for Australian matters and requirements where necessary to meet the needs of Australian stakeholders; and

- in alignment with the Australian Government’s direction to address climate-related financial disclosures first, to develop climate-related financial disclosure requirements that can be applied independently of any broader sustainability reporting framework.

As a result of the above decisions, the ASRS Exposure Draft includes a number of areas of departure from the IFRS Sustainability Disclosure Standards.

A high-level summary of the requirements of the IFRS Sustainability Disclosure Standards, and some key changes made by the AASB from the international standards are explored in more detail in this sustainability reporting alert.

A list of the main changes in the ASRS Exposure Draft is contained in the Appendix.

A COMPARISON OF DISCLOSURE REQUIREMENTS

This sustainability reporting alert is prepared as a summary of the key differences between the ASRS ED and IFRS Sustainability Disclosure Standards and does not cover every disclosure requirement of the IFRS Sustainability Disclosure Standards or Australian Sustainability Reporting Standards. Refer to the issued standards or the ASRS Exposure Draft for full detail of disclosure requirements and ASRS Exposure Draft changes.

IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information

Objective & application

The objective of this Standard is to disclose all information about sustainability-related risks and opportunities that could reasonably be expected to affect a company’s prospects.

IFRS S1 provides the basic requirements for sustainability disclosures, which should be used with IFRS S2 as well as the future Standards that the ISSB releases. Future potential topical standards identified by the ISSB include nature and biodiversity, human capital and human rights.

The IFRS Sustainability Disclosure Standards were issued primarily to be applied by for-profit entities and designed to meet the needs of investors. As such, it requires an entity to disclose information that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term.

Key ASRS Exposure Draft differences

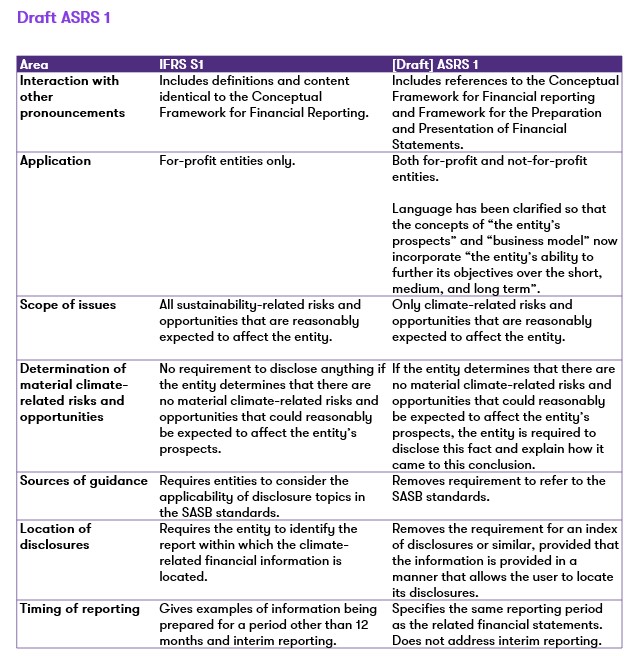

The AASB is proposing to modify the application of the ASRS to also be applicable to not-for-profit entities.

As a result it has defined the objective of the ASRS is to disclose information about climate-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, access to finance or cost of capital, and its ability to further its objectives, over the short, medium or long term.

Conceptual foundations and general requirements

The standard defines some core reporting concepts including:

- sustainability-related financial information;

- fair presentation;

- materiality;

- the reporting entity;

- connectivity of information;

It also outlines general requirements in relation to:

- location of disclosures;

- timing of reporting;

- comparative information;

- judgements;

- measurement uncertainty; and

- the correction of prior period errors.

Key ASRS Exposure Draft differences

There are no significant changes to the conceptual foundations proposed in the ASRS, however the AASB has made some clarifications in relation to the location of disclosures and timing of reporting.

Identifying sustainability-related risks and opportunities

The first step of applying IFRS S1 requires the entity to identify all sustainability-related risks and opportunities that are reasonably expected to affect the entity, and to disclose material information about these risks and opportunities.

In identifying the sustainability-related risks and opportunities, and the material information to disclose, requires the entity to consider, in addition to the IFRS Sustainability Disclosure Standards:

- the Sustainability Accounting Standards Board Standards (SASB standards).

- other sources of guidance including:

- the Carbon Disclosures Standards Board Framework (CDSB Framework);

- the Global Reporting Initiative (GRI);

- the European Sustainability Reporting Standards (ESRS);

- industry practice; and

- any other standard setters or investor focused frameworks.

Key ASRS Exposure Draft differences

Unlike IFRS S1, the ASRS Exposure Draft requires:

- identification of material climate-related risks and opportunities only; and

- no requirement to consider the SASB standards or other sources of guidance listed in IFRS S1.

Four core pillars of disclosures

IFRS S1 establishes a disclosure framework under four key pillars, consistent with the Taskforce on Climate-related Financial Disclosures (TCFD) recommended disclosures:

![]()

- Governance: How the entity monitors and manages sustainability-related risks and opportunities;

- Strategy: The anticipated impact of sustainability-related risks on the business model, value chain, financial position and performance;

- Risk management: The processes used to identify, assess, and prioritise sustainability-related risks and opportunities, including the use of scenario analysis; and

- Metrics and Targets: Disclosure of sustainability-related metrics used to measure and manage its sustainability-related risks and opportunities, and progress towards any targets the entity has set.

Key ASRS Exposure Draft differences

There are no significant changes to the four pillars of disclosures proposed in the ASRS.

IFRS S2 Climate-related Disclosures

IFRS S2 is the first topic standard of the IFRS Sustainability Disclosure Standards, focused on material physical and transitional climate-related risks and opportunities.

The standard fully incorporates all 11 recommendations of the Taskforce on Climate-related Financial Disclosures (TCFD) but introduces incremental disclosures which are more granular, and prescriptive quantitative requirements. For entities that were previously disclosing in accordance with the TCFD recommendations, the IFRS Foundation has published a comparison of the requirements in IFRS S2 and the TCFD recommendations available on the IFRS Foundation website here.

The standard requires the entity to consider climate-related risks and opportunities, including physical risks (e.g. increased natural disasters), as well as transition risks (arising from moving to a lower-carbon economy), and the potential impact on their current and future financial position and performance.

Governance

IFRS 2 requires disclosures about the governance processes, controls and procedures an entity uses to monitor, manage and oversee climate-related risks and opportunities.

This includes disclosure of:

- Identification of the responsible individual or body for oversight of climate-related risks and opportunities, and make disclosures in relation to:

- how their responsibilities for climate-related risks and opportunities are reflected in the terms of reference, mandates, role descriptions and other related policies;

- how they determine whether appropriate skills and climate-competency are available, or will be developed;

- how and how often they are informed about climate-related risks and opportunities;

- how they take into account climate-related risks and opportunities when overseeing the entity’s strategy, decisions on major transactions and risk management processes;

- how they oversee the setting of climate-related targets and how they monitor progress towards the targets;

- whether, or how, climate-related performance metrics are integrated into their remuneration policies; and

- Management’s role in the governance of climate-related risks and opportunities, including:

- whether, or how, the role is delegated to management; and

- whether management uses controls and procedures to support them with its oversight function, and how these controls and procedures are integrated with other internal functions.

Key ASRS Exposure Draft differences

The AASB has clarified the requirement to disclose whether or how climate-related performance metrics are integrated into remuneration policies, is made in relation to key management personnel remuneration. This is based on the application of AASB 124 Related Party Disclosures.

Strategy

IFRS S2 requires disclosures about an entity’s strategy for managing climate-related risks and opportunities.

This includes disclosure of:

- the climate-related risks and opportunities that could reasonably be expected to affect the entity’s prospects;

- the current and anticipated effects of those climate-related risks and opportunities on the entity’s business model and value chain;

- the effects of those climate-related risks and opportunities on the entity’s strategy and decision-making, including information about its climate-related transition plan;

- the effects of those climate-related risks and opportunities on the entity’s financial position, financial performance and cash flows for the reporting period, and their anticipated effects on the entity’s financial position, financial performance and cash flows over the short, medium and long term; and

- the climate resilience of the entity’s strategy and its business model to climate-related changes, developments and uncertainties.

The entity shall use climate-related scenario analysis to assess its climate resilience using an approach that is commensurate with the entity’s circumstances.

Key ASRS Exposure Draft differences

Unlike IFRS S2, the ASRS Exposure draft requires that, when assessing the climate resilience of the entity’s strategy and business model, the climate-scenario analysis shall:

- at minimum include two scenarios of possible future states; and

- one of the scenarios must be aligned to the most ambitious global temperature goal set out in the Climate Change Act 2022 (currently a 1.5 degree scenario).

Risk Management

IFRS S2 requires disclosures about an entity’s processes to identify, assess, prioritise and monitor climate-related risks and opportunities, including whether and how those processes are integrated into and inform the entity’s overall risk management process.

This includes disclosure of:

- the processes and related policies the entity uses to identify, assess, prioritise and monitor climate-related risks;

- the processes the entity uses to identify, assess, prioritise and monitor climate-related opportunities;

- whether and how the entity uses climate-related scenario analysis to inform its identification of climate-related opportunities; and

- the extent to which, and how, the processes for identifying, assessing, prioritising and monitoring climate-related risks and opportunities are integrated into and inform the entity’s overall risk management process

Key ASRS Exposure Draft differences

There are no significant changes to the risk management required disclosures proposed in the ASRS Exposure Draft.

Metrics and Targets

IFRS S2 requires disclosure of metrics and targets to enable an understanding of an entity’s performance in relation to its climate-related risks and opportunities, including progress towards any climate-related targets it has set, and any targets it is required to meet by law or regulation.

This includes disclosure of:

- cross-industry metric categories, comprising:

- gross greenhouse gas emissions (Scope 1, 2 & 3);

- the amount and percentage of assets or business activities vulnerable to climate-related transition risks;

- the amount and percentage of assets or business activities vulnerable to climate-related physical risks;

- the amount and percentage of assets or business activities aligned with climate-related opportunities;

- the amount of capital expenditure, financing or investment deployed towards climate-related risks and opportunities;

- whether and how the entity is applying a carbon price in decision-making, and the price used;

- the percentage of executive management remuneration recognised in the reporting period that is linked to climate-related considerations;

- industry-based metrics that are closely associate with particular business models, activities or other common features that characterise participation in an industry; and

- targets set by the entity, and any targets it is required to meet by law or regulation.

Key ASRS Exposure Draft differences

Greenhouse gas emissions measurement

Unlike IFRS S2, the ASRS Exposure Draft requires that:

- greenhouse gas emissions are calculated by applying relevant methodologies and global warming potential values (GWP values) set out in NGER Scheme legislation, to the extent practicable, before applying other methodologies;

- introduces a measurement hierarchy to be applied when measuring greenhouse gas emissions; and

- adds accompanying Australian Application Guidance to explain this measurement hierarchy.

Scope 2 emissions

For scope 2 emissions (indirect emissions from the generation of purchased energy consumed by the entity), the ASRS Exposure Draft adds an incremental disclosure requirement to disclose Scope 2 emissions calculated using a market-based approach.

Scope 3 emissions

For scope 3 emissions (indirect emissions occurring upstream and downstream in the entity’s value chain), the ASRS Exposure Draft introduces the ability to disclose Scope 3 emissions using data from the immediately preceding reporting period, if reasonable and supportable data for the reporting period is not available to the entity without undue cost or effort.

Industry-based metrics

The ASRS Exposure Draft has no requirement to consider the SASB standards, and therefore does not require specific industry-based metrics.

If an entity wants to disclose a well-established and understood metric associated with a particular industry, then the entity must apply the Australian and New Zealand Standard Industrial Classification system (ANZSIC).

Draft ASRS 101 Reference in Australian Sustainability Reporting Standards

ASRS 1 & ASRS 2 make references to a number of external documents or sources of guidance not contained in the ASRS standards, which over time may be updated or amended.

To enable these external documents to have the same authoritative status as the standards [Draft] ASRS 101 has been developed to list the relevant versions of non-legislative external documents referenced, both foreign and domestic. The documents and the specific versions listed in [Draft] ASRS 101 are required to be applied by an entity to the extent required by the ASRS in order to claim compliance with the ASRS Standards.

International compliance considerations

The changes introduced in the ASRS Exposure Draft are sufficiently substantive it would not be unusual that compliance with the ASRS would preclude compliance with the IFRS Sustainability Disclosure Standards.

For entities that may report under multiple sustainability reporting frameworks, it is important to:

- identify the other sustainability reporting framework(s) applicable to the entity;

- identify any different or incremental reporting requirements for compliance with other framework(s); and

- discuss with the entity’s auditors how the different or incremental reporting requirements will be met and reported.

Based on the exposure draft legislation of amendments to the Corporations Act, the ASRS Sustainability Report will be subject to assurance. As such clear demarcation between the ASRS Sustainability Report disclosure requirements and any other disclosures made that are not subject to assurance is likely to be necessary.

APPENDIX: CHANGES IN THE AUSTRALIAN EXPOSURE DRAFTS

![]()

Download

FURTHER INFORMATION

If you wish to discuss any of the information included in this Sustainability Reporting Alert, please get in touch with your local Grant Thornton Australia contact or a member of the Sustainability Reporting team at sustainability.reporting@au.gt.com.