Our audit team undertakes the complete range of audits required of Australian accounting laws to help you to help you meet obligations or fulfil best practice procedures.

In this episode, Partner and Head of Digital Assurance Liam Te-Wierik explores how technology is assisting auditors, the guardrails to be considered when using these tools and his thoughts on future trends for the auditing profession.

We help clients understand and address their employment tax obligations to ensure compliance and optimal tax positioning for their business and employees.

In this episode, Corporate Tax Partner Vince Tropiano, Global Trade Partner Richard Nutt and Innovation Incentives Director Simone Barker discuss the Australian economy and how tariffs are impacting Australian manufacturing businesses – and what they can do to mitigate risks.

We provide independent oversight and review of your organisation's control environments to manage key risks, inform good decision-making and improve performance.

We enable our clients to achieve their strategic objectives, fulfil their purpose and live their values supported by effective and appropriate risk management.

Last week, the Australian Securities and Investments Commission (ASIC) released a report highlighting issues with the superannuation industry's handling of death benefit claims and the impact these have on grieving Australians.

Our forensics team identifies and obtains relevant information, investigates the financial issue at hand and provides a clear, concise, sustainable opinion as...

Our team advises at all stages of a litigation dispute, taking an independent view while gathering and reviewing evidence and contributing to expert reports.

Post-acquisition disputes can significantly impact the success of a transaction and the ongoing success of the businesses involved. Read about practical insights into common post-acquisition dispute issues and how to address them proactively, particularly through the financial due diligence and deal advisory process.

Our M&A team works with clients to achieve a full or partial sale of their business, to ensure achievement of strategic ambitions and optimal outcomes for stakeholders.

Our operational deal services team helps to ensure the greatest possible outcome and value is gained through post merger integration or post acquisition integration.

As environmental, social, and governance (ESG) considerations become increasingly pivotal for dealmakers in Australia, it is important for investors to feel confident in assessing transactions through an ESG lens.

Post-acquisition disputes can significantly impact the success of a transaction and the ongoing success of the businesses involved. Read about practical insights into common post-acquisition dispute issues and how to address them proactively, particularly through the financial due diligence and deal advisory process.

Our finance and funding team works to access sources of finance, present your case to potential funders and negotiate a long-term sustainable relationship.

We provide effective and strategic corporate finance services across all stages of investments and transactions so clients can better manage costs and maximise returns.

We work closely with clients and lenders to provide holistic debt advisory services so you can raise or manage existing debt to meet your strategic goals.

Our proven methodology identifies opportunities to improve your processes and optimise working capital, and we work with to implement changes and monitor their effectiveness.

The biotech industry faces significant challenges, including regulatory pressures, supply chain disruptions, rising costs and shifting investment landscapes.

Our insolvency teams takes a proactive approach so our clients have access to more business turnaround options and retain the most value for all stakeholders.

Rising costs, supply chain disruptions, and shifting consumer behaviour are pushing many retailers to the edge. Taking immediate action to reduce operational expenses and prioritise cash flow management can give businesses the breathing room they need. Retailers must adapt quickly to survive these challenging market conditions and avoid insolvencies.

We help clients improve commercial performance, profitability and address challenges after internal or external triggers require a major business model shift.

We provide strategic director advisory services in times of business distress to help directors navigate issues and protect their company and themselves from liability.

We work closely with clients and lenders to provide holistic debt advisory services so you can raise or manage existing debt to meet your strategic goals.

Rising costs, supply chain disruptions, and shifting consumer behaviour are pushing many retailers to the edge. Taking immediate action to reduce operational expenses and prioritise cash flow management can give businesses the breathing room they need. Retailers must adapt quickly to survive these challenging market conditions and avoid insolvencies.

We work with private businesses across Australia – and internationals looking to Australia for their investments and operations – on all accounting and...

Our outsourced CFO services provide a full suite of CFO, tax and finance services and advice to help clients manage risk, optimise operations and grow.

Having a considered and informed ESG response has never been more important for all organisations as we are seeing awareness of the elements of ESG continue to...

There is a growing demand for organisations to provide transparency on their commitment to sustainability and disclosure of the nonfinancial impacts of their business activities. Commonly, the responsibility for sustainability and ESG reporting is landing with CFOs and finance teams, requiring a reassessment of a range of reporting processes and controls.

With the ESG and sustainability landscape continuing to evolve, we are focussed on helping your business to understand what ESG and sustainability represents and the opportunities and challenges it can provide.

As the demand for organisations to prepare information in relation to ESG & sustainability continues to increase, through changes in regulatory requirements or stakeholder expectations, there is a growing need for assurance over the information prepared.

As environmental, social, and governance (ESG) considerations become increasingly pivotal for dealmakers in Australia, it is important for investors to feel confident in assessing transactions through an ESG lens.

The purpose of this Alert is to draw attention to Regulatory Guide RG 280 Sustainability reporting (RG 280 or regulatory guide), published by the Australian Securities and Investment Commission (ASIC) on 31 March 2025.

In the dynamic landscape of family business and current economic environment, it’s critical to prepare the next generation to ensure they’re comfortable to take over operations.

Investment and business opportunities in Vietnam are expanding rapidly, driven by new markets, diverse industries, and Vietnam's growing role in export manufacturing, foreign investment, and strong domestic demand.

Treasury is taking steps to ensure fairer tax treatment for foreign resident investors by tightening Australia's foreign resident Capital Gains Tax (CGT) regime. Proposed changes aim to broaden the CGT base and enhance integrity, impacting infrastructure, energy, agriculture, and more.

If government grants are part of your 2025 strategy, take note of the available quarter one funding opportunities. With increasing inflationary pressures, government grants can be an essential alternative funding source for businesses with critical investment projects.

Merger & Acquisition (M&A) and equity market activity in the Agribusiness, Food & Beverage (Ag, F&B) sector is undergoing a strategic shift, as investors have become more selective and increasingly cautious in response to global economic uncertainty.

Treasury is taking steps to ensure fairer tax treatment for foreign resident investors by tightening Australia's foreign resident Capital Gains Tax (CGT) regime. Proposed changes aim to broaden the CGT base and enhance integrity, impacting infrastructure, energy, agriculture, and more.

From an active natural resources M&A market, a growing energy and renewable energy market, to new technologies and export and trade agreements – we have the...

As of April 9, 2025, a minimum universal tariff of 10 per cent has been applied to all imported goods into the United States, while certain countries face higher reciprocal tariffs based on their US trade deficit.

At Grant Thornton we do things differently because we understand that when you strive for better and care about what you do remarkable things are possible.

The compelling client experience we’re passionate about creating at Grant Thornton can only be achieved through our people. We’ll encourage you to influence how, when and where you work, and take control of your time.

At Grant Thornton, we strive to create a culture of continuous learning and growth. Throughout every stage of your career, you’ll to be encouraged and supported to seize opportunities and reach your full potential.

To be able to reach your remarkable, we understand that you need to feel connected and respected as your authentic self – so we listen and strive for deeper understanding of what belonging means.

We’re passionate about making a difference in our communities. Through our sustainability and community engagement initiatives, we aim to contribute to society by creating lasting benefits that empower others to thrive.

As a new graduate, we aim to provide you more than just your ‘traditional’ graduate program; instead we kick start your career as an Associate and support you to turn theory into practice.

Commencing in 2021, the Federal Government has announced a new, simplified small business restructuring process for small businesses as part of the economic relief reforms.

The Small Business Restructuring Process (“SBRP”) is designed to assist businesses restore operational liquidity by severing the financial burden of legacy debts through a formal debt compromise with creditors.

Unlike other formal restructuring procedures, the SBRP allows for Company Directors to remain in control of and continue to trade their business during the restructuring period.

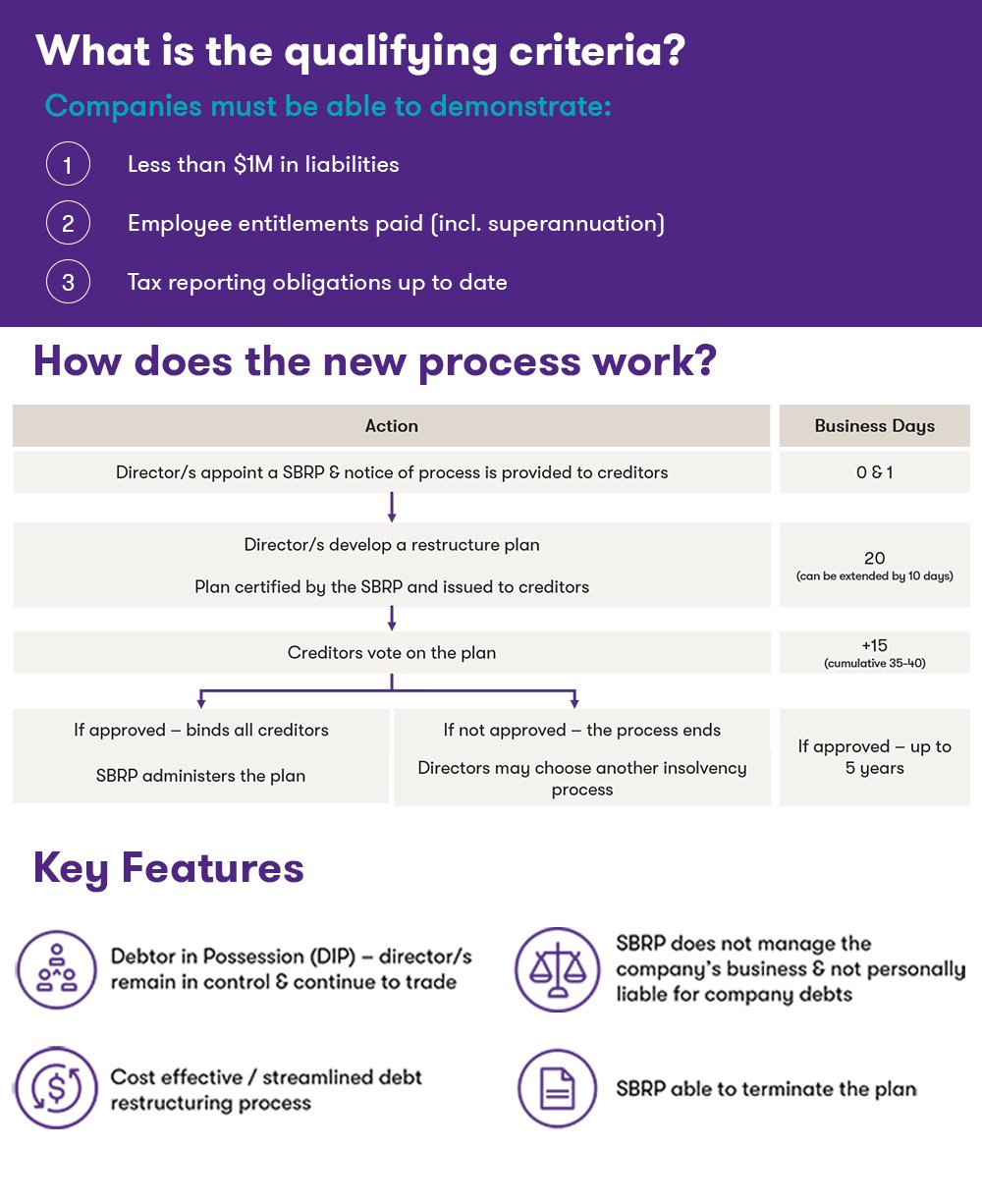

Qualifying for the SBRP

Companies wishing to utilise this process must be able to demonstrate the following:

less than $1 million in liabilities (excluding liabilities to employees of the Company);

all outstanding employee entitlements, including superannuation, must have been paid (nb. this does not include entitlements not yet due for payment, such as annual or long service leave); and

all tax lodgements for the company must be up to date.

Developing a plan: How does the new process work?

On commencement of the engagement of a small business restructuring practitioner (“SBR practitioner”), all unsecured and some secured creditors (eg Retention of Title and Lessors) are prohibited from taking action against the company to recover money and/or collect property (including terminating contracts and formal debt recovery proceedings).

Over the next 20 business days, the Company’s Directors (working with the SBR practitioner) develop a plan to restructure the company’s unsecured creditor debts and collate relevant documents to support the plan, which will ultimately be for creditor consideration. Typically, a plan creates a pool of monies which is applied in full and final settlement of all unsecured creditor debts, excluding related party debt that existed at the time of entering the SBRP. The pool of monies could be funded from various sources, including:

third party contributions

proceeds from the sale of assets

future trading profits

refinance

As a tool to compromise creditor claims, the funding pool does not need to provide for the payment of creditor claims in full. The circumstances of each case will determine the necessary structure and quantum of the funding pool. In almost all cases, the outcome to creditors should be greater than the expected return if the Company were to be placed in Liquidation.

At or before the end of the 20 business days, the SBR practitioner certifies the plan based on their assessment of the Company’s financial affairs and issues the plan to creditors for their consideration.

After receiving the plan, creditors have 15 business days to vote on the plan. If more than 50% in value of unrelated creditors that participate in the vote support the plan, it is approved and binds all unsecured creditors.

If the plan is approved, the business continues to trade under the control of the Directors and the practitioner administers the plan and distributes funds to creditors.

Whilst a rejection of the plan does not necessarily lead to a Liquidation of the Company, the Directors may need to consider the ability to continue trading the Company if it is unable to demonstrate viability.

During the restructuring period, a personal guarantee cannot be enforced against a Director or one of their relatives.

During the restructuring process, the Company’s Directors retain control of the company, which in turn helps to minimise costs and business disruption. We expect that, in most cases, the professional fees for conducting a SBRP will be less than the cost of conducting a more traditional external administration (such as a Voluntary Administration or Liquidation).

The professional fee of the restructuring professional for developing the restructuring plan and liaising with creditors about the SBRP is agreed and fixed up-front.

Our experience is that most SMEs find it difficult, costly and commercially embarrassing to pursue a path of agreeing an informal compromise with creditors.

The ATO is more often than not a significant creditor in corporate insolvencies, however the ATO’s policy on compromising debts (other than penalties and interest) outside of an external administration is quite onerous and difficult to satisfy.

The SBRP provides a simple and cost-effective procedure for companies with unmanageable legacy debts to settle those and other debts, while at all times retaining control of the Company and its business.

A wrap up. What does this mean for key stakeholders?

Advisors to small businesses should be aware that while on its face the SBRP may appear an attractive proposition, failure to properly consider key stakeholder concerns (funding continued supply, lender support and recapitalisation sources) prior to formally entering into a SBRP could result in business failure rather than rescue.

For more information on insolvency reforms to support small business please see:

Rising costs, supply chain disruptions, and shifting consumer behaviour are pushing many retailers to the edge. Taking immediate action to reduce operational expenses and prioritise cash flow management can give businesses the breathing room they need. Retailers must adapt quickly to survive these challenging market conditions and avoid insolvencies.

As this year’s series kicks off in late 2024, continuing through to June 2025, we will bring you virtual on-demand webinars featuring guest speakers, legal and industry experts, and Grant Thornton specialists sharing insights and expectations for the year ahead.

In the latest episode of Beyond the Numbers with Grant Thornton, Financial Advisory Partners John McInerney and Cameron Crichton discuss the current economic climate, what SBRs are, eligibility criteria, and how businesses have successfully turned around using this regime.

Subscribe now to be kept up-to-date with timely and relevant insights, unique to the nature of your business, your areas of interest and the industry in which you operate.