The economy grew 4.2 per cent in 2021 and is poised for a similar expansion in 2022. Australia’s better-than predicted economic recovery has created a red-carpet lead-in to the 2022-23 Federal Budget on 29 March 2022 and the Federal Election to take place by 21 May.

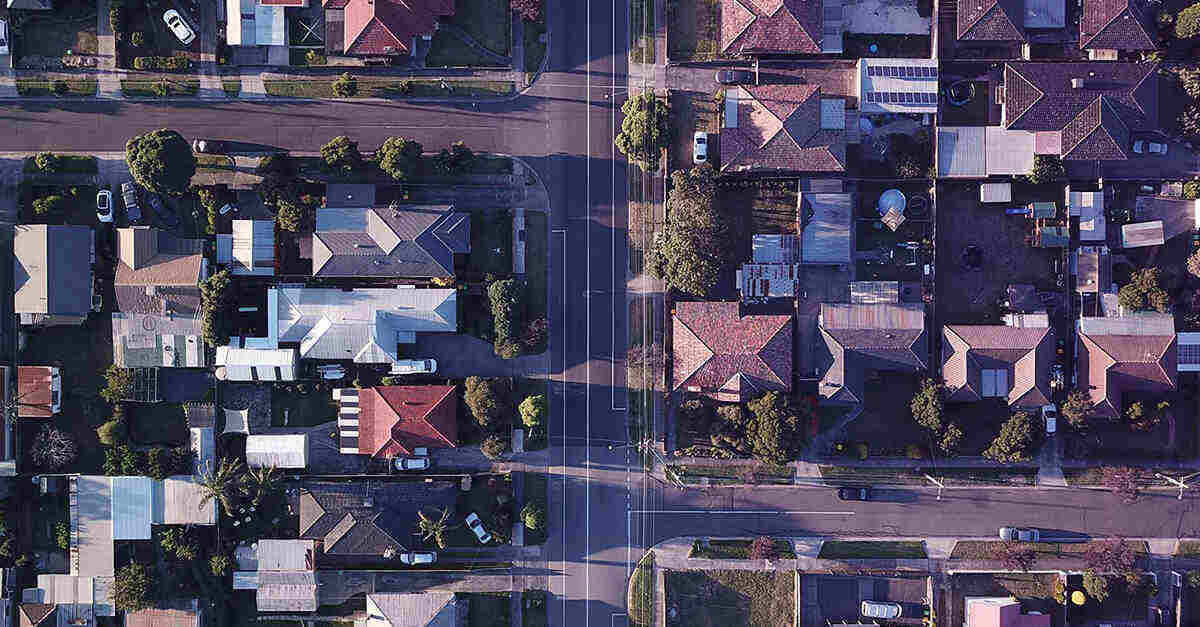

However, a less desirable title Australia has been trying to shake off, with little success – is our ranking as one of the least affordable housing nations in the world. Despite border closures halting international migration and state-based restrictions limiting interstate movement, Australia’s housing market again took off in 2021.

Nationally, house values rose almost 25 per cent – a boon for the 67 per cent of Australians with a stake in the property market. However, the heat appears to be coming off, particularly in Sydney and Melbourne, while regional Australia is continuing to benefit from the city price squeeze, according to CoreLogic’s February 2022 report.

Which groups are in most need of more affordable housing?

While property owners enjoy extraordinary capital gains, there are still 1 in 3 Australians in rental accommodation, including those aspiring to own their own home.

The great Australian dream continues to be an elusive aspiration, most notably for younger generations. Between 1971 and 2016, home ownership rates for 30–34-year-olds declined by 14 percent to 50 per cent. Similarly, rates for 25–29-year-olds also dropped by 13 per cent to 37 per cent, according to Australia Bureau of Statistics (ABS) Census data.

Retirees who don’t own their own homes are also doing it tough. A recent CHOICE survey found that over 200,000 retired Australians who are currently renting their home are living below the poverty line, with many going without essentials like food and transport to make ends meet. But even if the Government raised its current Rent Assistance by 40 per cent, of this group, only roughly 14 per cent would be lifted out of income poverty.

Housing inequality is also deepening. About 150,000 households are currently on social housing waiting lists, while the number of people who identified as homeless in the 2016 Census rose to 116,000 Australians – a 14 per cent increase on 2011. Results from the 2021 Census, which the ABS will start releasing from June 2022, will provide a more current picture on homelessness in Australia, and any new trends that have emerged because of the pandemic. The outcomes are not predicted to be positive.

Who is building affordable housing?

Private developers and not-for-profits are continuing to leverage new and existing opportunities to meet Australia’s housing needs, despite facing labour shortages, supply chain issues and high material costs – costs that could be further exacerbated by the distressing Ukraine conflict and extreme weather events.

The construction industry – our economic powerhouse – has continued to operate through the pandemic and has played a critical role in Australia’s economic recovery. Industry players are also exploring more creative housing supply opportunities. Successful overseas property solutions, such as build-to-rent developments, are gaining momentum in Australia with this new asset class attracting increasing capital investment from institutional backers and support from State Governments.

Not-for-profits are also stepping up to address Australia’s housing gap, leveraging opportunities through the Australian Government’s National Housing Finance and Investment Corporation (NHIC). According to the corporation, in the three years since its inception, it has approved “$2.8 billion in long-term loans to 35 Community Housing Providers (CHP), supporting over 14,000 new and existing homes and saving these CHPs an estimated $470 million in interest and fees as well as other indirect costs associated with refinancing.”

What could the Government propose in this year’s Budget to help create more affordable housing?

Despite these measures, housing affordability remains a persistently stubborn policy thorn for all governments. It has been the subject of several national inquiries, including a new parliamentary inquiry initiated by Federal Treasurer Josh Frydenberg last year. The Standing Committee on Tax and Revenue is due to present its findings on the contribution of tax and regulation to housing affordability and supply to Parliament in the first half of 2022. The 160 submissions made to the inquiry tell a familiar story about the complex interplay between dwelling supply and demand; housing inequality; fiscal and monetary settings, including interest rates; population demographics and household profiles; urban planning; land availability; and Australia’s complex three-tier regulatory environment.

Depending on the timing of the release of the inquiry’s findings, the Australian Government’s response may signal its Budget and future policy intentions on the issue. However, Prime Minister Scott Morrison’s reported comments at the annual Master Builders National Leaders Election Summit in February – that rising house prices reflected ‘how the market works’ – appeared to indicate a lack of political appetite for major reform.

The policy levers available to the Commonwealth to significantly influence housing affordability are limited compared with the avenues of reform available to its state and territory counterparts. However, the government has already pulled a number of them in past budgets.

It has lifted the voluntary contributions first home buyers can access under the First Home Super Saver Scheme from $30,000 to $50,000 from 1 July 2022. The NHIC is already well established as a national reform vehicle to address housing affordability issues and could therefore attract further Budget investment. In addition to increasing housing supply, the corporation also administers the Australian Government’s first-home buyer and single parent home purchase assistance schemes.

Like many other countries, the Commonwealth has tightened controls on foreign investment in residential property in a bid to strike the right balance between encouraging foreign investment for the purpose of generating new stock, while also protecting the ability of Australians to access housing.

While new data on foreign purchases and sales of residential real estate released by the Foreign Investment Review Board (FIRB) doesn’t reflect the latest changes, it does provide useful insights and trend data.

The report showed almost 7,500 properties valued at $6 billion were purchased with a level of foreign ownership in 2019-2020. In comparison, sales involving foreign owners over the same period totalled 1,957 with a value of $1.5 billion dollars. Unsurprisingly, the overwhelming majority of all transactions occurred in Victoria, New South Wales and Queensland. The data showed purchases declined over a three-year period to their lowest level in 2019-2020 as sales reached their highest point in the same year. While the data only incorporates the very start of the COVID-19 impact, the decline in purchase transactions demonstrates that the FIRB changes around application fees in 2015 and foreign surcharges imposed at a state level on residential acquisitions have had an impact.

While there is significant interest in the economic narrative and funding priorities of the 2022-23 Federal Budget, after its release all eyes will quickly turn to the Reserve Bank, whose decisions in 2022 could have a broader and deeper impact on future housing supply, construction and owner and purchaser intentions.